Main Content

Newland Real Estate

Featured Listings

Welcome To Newland Real Estate

Real Estate

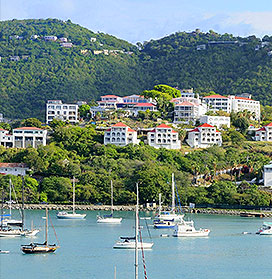

It is with great pleasure that April welcomes you to the Virgin Islands. With years of experience in the market, she knows how crucial it is for you to find relevant, up-to-date information. The search is over. Her website is designed to be your one-stop shop for real estate in the Virgin Islands.

This is the moment that you should enjoy the most; looking at the available properties in the Virgin Islands; imagining yourself living in the home that you have always dreamed about. You don’t want just another database that gives you rehashed property descriptions. You want to walk around the neighborhood from the comfort of your own home. You want to get a clear picture about life in the Virgin Islands.

Read More

Our History

- This is the moment that you should enjoy the most; looking at the available properties in the Virgin Islands.

- Imagining yourself living in the home that you have always dreamed about.

- You don’t want just another database that gives you rehashed property descriptions.

- You want to walk around the neighborhood from the comfort of your own home.

- You want to get a clear picture about life in the Virgin Islands.

Featured Areas

QTR

QTR

NORTHSIDE

QTR

NORTHSIDE

QTR

Marienhoj

QTR

QTR

northside

QTR

northside

QTR

Sherpenjewel

Rosendahl

Welgonski

Fancy

Quarter

Bay QTR

Bay QTR

QTR

QTR

Harmony

QTR

QTR

Our Team Trusted In The Business

That is exactly what you get here. This website has been built with you in mind. From the highest quality property images to the most informative guides and blogs, she is here to make your home buying or selling experience smooth and stress-free.

Meet The Team